In today’s evolving financial landscape, borrowers in India are no longer limited to traditional banks when seeking loans. The rise of Non-Banking Financial Companies (NBFCs) and digital lending platforms has significantly expanded the choices available to individuals and businesses. While this increased competition has made borrowing more accessible, it has also created confusion—especially when deciding between banks and NBFCs.

Choosing the right lender is just as important as choosing the right loan. Each option comes with its own set of advantages, limitations, and suitability depending on your financial profile, urgency, and borrowing needs. Making the wrong choice can lead to higher costs, stricter repayment conditions, or unnecessary delays.

This guide will help you understand the key differences between banks and NBFCs and determine which option is best suited for your needs.

Understanding Banks and NBFCs

Banks are traditional financial institutions regulated by the Reserve Bank of India (RBI) that offer a wide range of services, including savings accounts, credit cards, and loans. They are known for their stability, lower interest rates, and strict compliance standards.

NBFCs, on the other hand, are financial institutions that provide banking-like services but do not hold a banking license. They are also regulated by RBI but operate with more flexibility in lending practices. NBFCs have gained popularity due to their faster approval processes and relaxed eligibility criteria.

While both banks and NBFCs serve the same purpose of providing credit, their approach to lending is quite different.

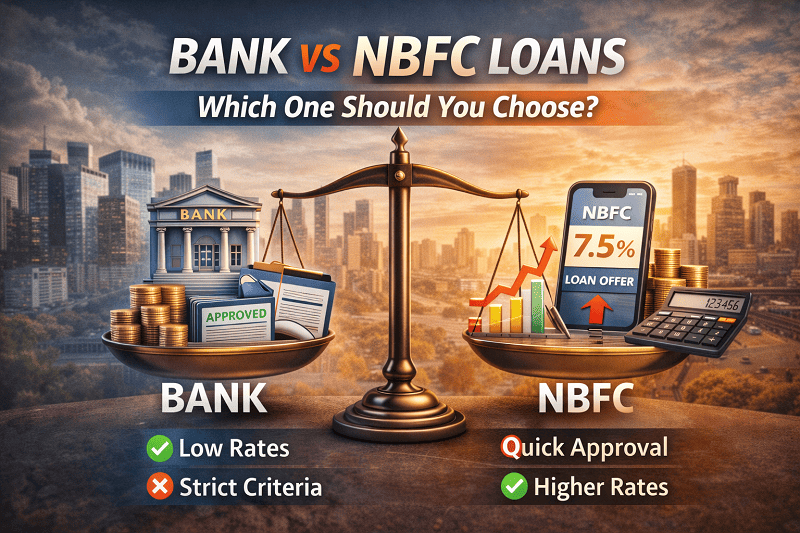

Interest Rates: Stability vs Accessibility

One of the biggest factors borrowers consider is interest rates. Banks generally offer lower interest rates compared to NBFCs because they have access to low-cost funds through deposits. This makes bank loans more affordable in the long run.

NBFCs, however, tend to charge slightly higher interest rates. This is because they take on higher risk by lending to individuals who may not meet strict bank criteria. While the rates may be higher, NBFCs provide access to credit for those who might otherwise struggle to get approved.

If you have a strong credit profile and meet bank eligibility criteria, a bank loan is often the cheaper option. But if accessibility is your priority, NBFCs can be a practical choice.

Eligibility Criteria: Strict vs Flexible

Banks typically have strict eligibility requirements. They prefer applicants with stable income, strong credit scores, and clear financial records. Salaried individuals working with reputed organizations and businesses with established financial history are more likely to get approved.

NBFCs, in contrast, offer more flexibility. They cater to a wider audience, including self-employed individuals, freelancers, and those with moderate or even low credit scores. This makes NBFCs a preferred option for borrowers who may not qualify for bank loans.

If your financial profile is strong, banks can offer better terms. But if you fall outside traditional criteria, NBFCs provide an alternative route to access funds.

Loan Approval Speed: Time vs Convenience

When it comes to processing time, NBFCs have a clear advantage. Banks often have longer approval cycles due to extensive documentation and verification processes. This can take several days or even weeks.

NBFCs, especially digital lenders, focus on speed and convenience. Many offer instant approvals and quick disbursal, sometimes within hours. This makes them ideal for urgent financial needs.

If time is not a constraint, banks offer better value. But if you need funds quickly, NBFCs are the better choice. Check social media handles of banks for latest loan offers.

Documentation and Process

Banks usually require detailed documentation, including income proof, bank statements, employment details, and credit history. The process is thorough but can be time-consuming.

NBFCs simplify the process by minimizing documentation requirements. Many lenders offer fully digital applications, reducing paperwork and making the process more user-friendly.

For borrowers who prefer a hassle-free experience, NBFCs provide a smoother journey. However, those willing to go through a detailed process may benefit from the lower rates offered by banks.

Loan Amount and Tenure Flexibility

Banks often provide higher loan amounts and longer tenures, especially for secured loans like home loans or business loans. Their structured approach ensures stability and predictability.

NBFCs, while flexible, may have limitations on loan amounts depending on the borrower’s profile. However, they offer more customized solutions, allowing borrowers to tailor repayment terms based on their needs.

If you require a large loan with long tenure, banks are usually the better option. For smaller, flexible loans, NBFCs work well.

Risk Assessment and Approval Chances

Banks follow a conservative approach to risk assessment. They prioritize applicants with strong financial backgrounds and low risk profiles. This reduces the chances of default but also limits access for many borrowers.

NBFCs adopt a more inclusive approach. They use alternative methods to assess creditworthiness, making it easier for individuals with non-traditional income sources to get loans.

This difference in approach is why NBFCs play a crucial role in financial inclusion in India.

Customer Experience and Support

Banks are known for their structured processes but may sometimes lack personalized service due to their scale and rigid systems. Customer support can vary depending on the institution.

NBFCs, especially newer digital platforms, focus heavily on customer experience. They offer user-friendly interfaces, quick responses, and personalized services.

For borrowers who value convenience and responsiveness, NBFCs often provide a better experience.

Hidden Charges and Transparency

Transparency is a critical factor when choosing a lender. Banks are generally more transparent with their charges and follow strict regulatory guidelines.

NBFCs, while competitive, may sometimes include additional charges such as processing fees, prepayment penalties, or service fees. It is important to read the terms carefully before making a decision.

Comparing the total cost of the loan rather than just the interest rate helps avoid surprises later.

When Should You Choose a Bank?

Banks are the right choice when you have a strong financial profile, stable income, and time to go through a detailed application process. They are ideal for borrowers looking for lower interest rates, higher loan amounts, and long-term financial stability.

If you are planning a major financial commitment, such as a home loan or business expansion, banks provide a more structured and cost-effective solution.

When Should You Choose an NBFC?

NBFCs are best suited for borrowers who need quick access to funds, have flexible income structures, or may not meet strict bank criteria. They are ideal for personal loans, short-term financial needs, and situations where speed is critical.

For individuals who value convenience and accessibility, NBFCs offer a practical alternative.

The Smart Approach: Compare Before You Choose

In 2026, the smartest way to choose between banks and NBFCs is not to pick one blindly but to compare multiple options before making a decision. Each lender offers different terms, rates, and benefits, and the best choice depends on your specific needs.

Using comparison platforms allows you to evaluate offers side by side, ensuring that you get the best deal without compromising on important factors.

Avoid Common Borrowing Mistakes

Many borrowers make the mistake of choosing lenders based on convenience alone. Others focus only on interest rates without considering additional charges.

Some apply to multiple lenders simultaneously, which can negatively impact their credit score. Others fail to read the fine print, leading to unexpected costs later.

Being aware of these mistakes can help you make a more informed and confident decision.

Financial decisions, whether it’s choosing between a bank or NBFC loan, often influence broader lifestyle and spending choices. Borrowers today are not just focused on securing funds but also on how efficiently they can utilize them in their daily lives. For instance, investing in practical and space-saving solutions like a foldable table for home reflects a growing preference for smart, budget-conscious decisions that align with both financial planning and modern living needs.

Final Thoughts

The choice between banks and NBFCs ultimately depends on your financial situation, urgency, and priorities. Banks offer stability, lower costs, and structured processes, while NBFCs provide flexibility, speed, and accessibility.

There is no one-size-fits-all answer. The best loan is the one that aligns with your needs, budget, and long-term financial goals.

By carefully evaluating your options, comparing offers, and understanding the key differences, you can make a smart borrowing decision that supports your financial well-being.

In a competitive lending environment like India, knowledge is your biggest advantage. Take the time to research, compare, and choose wisely—because the right loan can empower your future, while the wrong one can hold you back.